Transcript

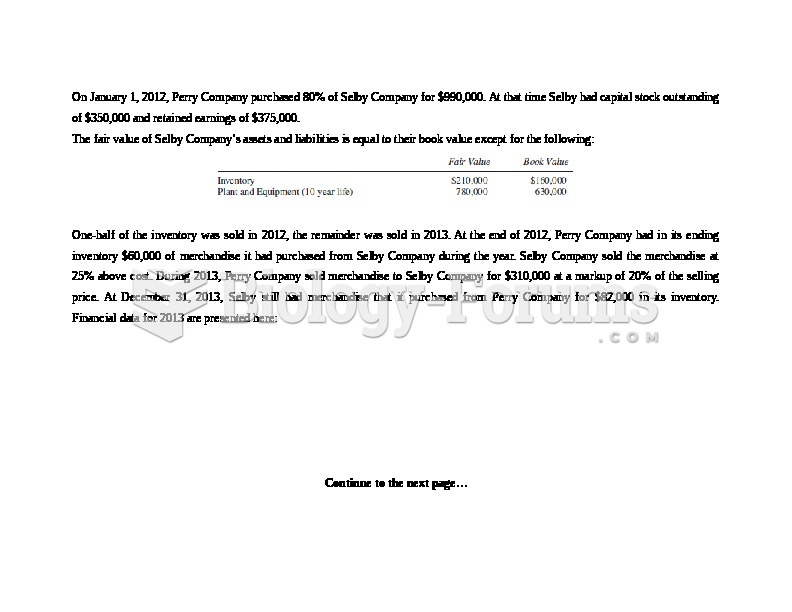

On January 1, 2012, Perry Company purchased 80% of Selby Company for $990,000. At that time Selby had capital stock outstanding of $350,000 and retained earnings of $375,000.

The fair value of Selby Company’s assets and liabilities is equal to their book value except for the following:

One-half of the inventory was sold in 2012, the remainder was sold in 2013. At the end of 2012, Perry Company had in its ending inventory $60,000 of merchandise it had purchased from Selby Company during the year. Selby Company sold the merchandise at 25% above cost. During 2013, Perry Company sold merchandise to Selby Company for $310,000 at a markup of 20% of the selling price. At December 31, 2013, Selby still had merchandise that it purchased from Perry Company for $82,000 in its inventory. Financial data for 2013 are presented here:

Continue to the next page…

Required:

A. Prepare the consolidated statements work-paper for the year ended December 31, 2013?

B. Calculate consolidated retained earnings on December 31, 2013, using the analytical or t-account approach?

SOLUTION

PERRY COMPANY AND SUBSIDIARY

Consolidated Statements Work-paper

Part A For the Year Ended December 31, 2013

Perry Selby

Eliminations Non-controlling Consolidated

Company Company

Debit

Credit Interest Balances

Income Statement

Sales $1,400,000 $800,000 (2) $310,000

$1,890,000

Dividend Income 20,000 (5) 20,000

Total Revenue 1,420,000 800,000

1,890,000

Cost of Goods Sold:

Inventory, 1/1 230,000 145,000 (7) 25,000 (4) 12,000

388,000

Purchases 900,000 380,000

(2) 310,000

970,000

Cost of Available for Sale 1,130,000 525,000

1,358,000

Inventory, 12/31 450,000 200,000 (3) 16,400

633,600

Cost of Goods Sold 680,000 325,000

724,400

Other Expense 250,000 195,000 (8) 15,000

460,000

Total Cost and Expense 930,000 520,000

1,184,400

Net/Consolidated Income 490,000 280,000

705,600

Noncontrolling Interest In Consolidated Income

50,400 * (50,400)

Net Income to Retained Earnings $490,000 $280,000 $386,400 $322,000 $50,400 $655,200

Retained Earnings Statement

1/1 Retained Earnings:

Perry Company $1,500,000

(4) $9,600 (1) $84,000

$1,542,400

(7) 20,000

(8) 12,000

Selby Company

480,000 (6) 480,000

Net Income from above 490,000 280,000

386,400

322,000 50,400 655,200

Dividends Declared

Perry Company (50,000)

(50,000)

Selby Company

(25,000)

(5) 20,000 (5,000)

12/31/ Retained Earnings to Balance Sheet $1,940,000 $735,000 $908,000 $426,000 $45,400 $2,147,600

* Non-controlling interest in income = .2 ($280,000 + $12,000 – $25,000 – $15,000) = $50,400

Perry Selby

Eliminations Non-controlling Consolidated

Company Company

Debit

Credit Interest Balances

Balance Sheet

Cash $ 95,000 $ 70,000

$ 165,000

Accounts Receivable 302,000 90,000

392,000

Inventory 450,000 200,000

(3) 16,400

633,600

Investment in Selby Comp. 990,000

(1) 84,000 (6) 1,074,000

Difference between Implied & Book Value

(6) 512,500 (7) 512,500

Plant and Equipment 850,000 585,000 (7) 150,000 (8) 30,000

1,555,000

Goodwill

(7) 312,500

312,500

Other Assets 390,000 230,000

620,000

Total Assets $3,077,000 $1,175,000

$3,678,100

Accounts Payable $ 75,000 $ 30,000

$ 105,000

Other Liabilities 102,000 60,000

162,000

Common stock:

Perry Company 960,000

960,000

Selby Company

350,000 (6) 350,000

Retained Earnings from above 1,940,000 735,000

908,000

426,000 45,400 2,147,600

1/1 Non-controlling Interest in Net Assets (4) 2,400 (6) 268,500 258,100

(7) 5,000

12/31 Non-controlling Interest in Net Assets

(8) 3,000

$303,500 303,500

Total Liabilities and Equity $3,077,000 $1,175,000 $2,327,400 $2,327,400

$3,678,100

Explanations of work-paper entries

Computation and Allocation of Difference Schedule

Parent Non- Entire

Share Controlling Value

Share

Purchase price and implied value $990,000 247,500 1,237,500 *

Less: Book value of equity acquired 580,000 145,000 725,000

Difference between implied and book value 410,000 102,500 512,500

Inventory ($210,000 - $ 160,000) (40,000) (10,000) (50,000)

Equipment ($780,000 - $ 630,000) (120,000) (30,000) (150,000)

Balance 250,000 62,500 312,500

Goodwill (250,000) (62,500) (312,500)

Balance -0- -0- -0-

*$990,000/.80

(1) Investment in Selby Company (0.80 ($480,000 – $375,000)) 84,000

Beginning Retained Earnings - Perry Co. 84,000

To establish reciprocity/convert to equity as of 1/1/13

(2) Sales 310,000

Purchases (Cost of Goods Sold) 310,000

To eliminate intercompany sales

(3) Ending Inventory - Income Statement (CoGS) 16,400

Ending Inventory (Balance Sheet) 16,400

To eliminate unrealized intercompany profit in ending inventory ($82,000 .2)

(4) Beginning Retained Earnings - Perry Co. ($12,000 .80) 9,600

Non-controlling Interest ($12,000 .20) 2,400

Beginning Inventory (Income Statement) 12,000

To recognize intercompany profit in beginning inventory realized during the year

($60,000 – ($60,000/1.25)) = $12,000

(5) Dividend Income ($25,000 .80) 20,000

Dividends Declared 20,000

To eliminate intercompany dividends

(6) Beginning Retained Earnings - Selby Co. 480,000

Common Stock - Selby Co. 350,000

Difference between Implied and Book Value 512,500

Investment in Selby Co. ($990,000 + $84,000) 1,074,000

Non-controlling Interest [$247,500 +.2 x ($480,000 – $375,000)] 268,500

(7) Equipment 150,000

Beginning Inventory (Income Statement) 25,000

Beginning Retained Earnings - Perry Co. 20,000

Non-controlling Interest 5,000

Goodwill 312,500

Difference between Implied and Book value 512,500

(8) Other Expenses (Depreciation) ($150,000/10) 15,000

Beginning Retained Earnings - Perry Co. 12,000

Non-controlling Interest 3,000

Equipment 30,000

Part B

Perry Company's Retained Earnings on 12/31/13 $1,940,000

Amount of Perry Company Retained Earnings that have not been realized in transactions with third parties (16,400)

Perry Company's Retained Earnings that have been realized in transactions with third parties 1,923,600

Increase in retained earnings of Selby Company from date of acquisition to 12/31/13 ($735,000 – $375,000) 360,000

Less: Cumulative effect of adjustments to date relating to amortization of the difference between implied and book value

($50,000 + $30,000) (80,000)

Less: Unrealized profit on sales to Perry in 2013 that has not been realized by sales to third parties 0

Increase in retained earnings of Selby Company since acquisition that has been realized in transactions with third parties 280,000

Perry Company's share (.80 $280,000) 80% 224,000

Consolidated Retained Earnings as of 12/31/13 $2,147,600

Consolidated Retained Earnings

Perry 's Share of unrealized profit on

Perry 's Retained Earnings on 12/31/13 $1,940,000

downstream sales to Selby

(in Selby's ending inventory),

Increase in Selby’s Retained Earnings

.2($82,000) 16,400 since acquisition ($735,000 - $375,000) = $360,000

Less: cumulative amortization of difference

between implied and book value 80,000

Adjusted Increase $280,000

Perry’s share thereof .80 224,000

Consolidated Retained Earnings $2,147,600