Transcript

COSTING /PRICING OF CB PRODUCTS

Major Issues and Challenges:

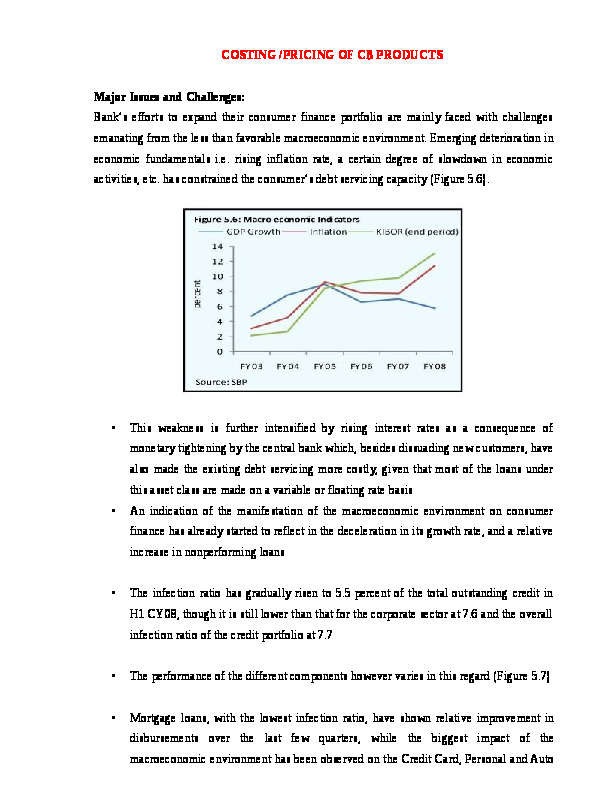

Bank’s efforts to expand their consumer finance portfolio are mainly faced with challenges emanating from the less than favorable macroeconomic environment. Emerging deterioration in economic fundamentals i.e. rising inflation rate, a certain degree of slowdown in economic activities, etc. has constrained the consumer’s debt servicing capacity (Figure 5.6).

1115695151130

This weakness is further intensified by rising interest rates as a consequence of monetary tightening by the central bank which, besides dissuading new customers, have also made the existing debt servicing more costly, given that most of the loans under this asset class are made on a variable or floating rate basis

An indication of the manifestation of the macroeconomic environment on consumer finance has already started to reflect in the deceleration in its growth rate, and a relative increase in nonperforming loans

The infection ratio has gradually risen to 5.5 percent of the total outstanding credit in H1 CY08, though it is still lower than that for the corporate sector at 7.6 and the overall infection ratio of the credit portfolio at 7.7

The performance of the different components however varies in this regard (Figure 5.7)

Mortgage loans, with the lowest infection ratio, have shown relative improvement in disbursements over the last few quarters, while the biggest impact of the macroeconomic environment has been observed on the Credit Card, Personal and Auto loans’ portfolio

Bank wise data shows that consumer loans are more concentrated in around 10 banks

Notwithstanding, since consumer credit is spread over a large number of borrowers, such risks are widely dispersed

Results of a stress testing exercise (based on end June CY08 data) conducted on banks’ consumer finance portfolio show that even a rise of 10.0 percentage points in the infection ratio will only reduce the Capital Adequacy Ratio (CAR) of banks by 90 bps

This is because the share of consumer finance in the overall credit extended by banks is still rather low at 12.0 percent

-2111375102870

In recognition of the underlying risks, SBP continues to make concerted efforts to strengthen the regulatory regime, as well as the risk management capacities of banks. The introduction of Prudential Regulations specifically designed to address the risk factors in the consumer finance portfolio in CY03, and enhancing the scope of the Credit Information Bureau (CIB) which was first launched in 1992 are some important measures implemented to ensure prudent growth of the portfolio. The enhancement in scope of the e CIB database now gives a comprehensive coverage of all borrowers of the banking sector (and some non bank financial institutions) which has helped banks in ensuring that customers are not over leveraged, and that the loan to income ratios are managed more prudently. Furthermore, SBP’s regulations and guidelines on risk management and internal controls effectively delineate the desirable level of internal controls and risk management capacities which the banks have started to implement for their consumer finance operations. Banks are building upon the existing capacities and rapidly improving their risk management expertise in response to regulatory requirements. Their progress along the learning curve suggests that they are now better placed to handle the challenges related to the operations of the consumer finance business.

Future Outlook

Given that the total consumer financing portfolio currently forms around 12.0 percent of the total loans and advances of the banking sector in comparison with substantially larger portfolios in peer countries, and its conducive role in promoting economic development, concerns about the potential risks of this product need to be viewed in perspective. This is particularly so because the household sector in Pakistan, from where the demand for consumer finance is generated, is financially sound and under leveraged by international standards.

Notwithstanding, given the pace of growth of this particular asset class and its increasing popularity, financial institutions need to carefully plan the expansion of their respective portfolios by minimizing the impact of the potential risks with adequate systems and resource support, in order to be able to sustain and positively avail the benefits of its growth.

Notwithstanding these developments, a few initiatives are still crucially needed for maintaining the stability of the consumer finance portfolio in coming years:

With the growing exposure against consumer finance, banks would need to implement specific credit scoring models. These can be based on the information derived from credit history databases, such as the turnaround time of monthly repayments, level of income and type of debt, length of credit relationship, in addition to other key pieces of information on social and demographic factors which help in establishing borrower profiles. The model will help banks in objectively identifying the credit worthiness of a borrower and the likely credit behavior. However, for building an effective credit scoring model, the existing databases on the consumer’s credit history would need significant enhancements;

The prevailing regime for enforcement of security liquidation and collection of debts needs to be rationalized in terms of effectiveness and fairness to both banks as well as consumers;

Considering the low level of financial literacy of the average consumer, mainly due to the low level of awareness and the prevailing literacy rate in the country, banks would need to review the transparency of the pricing mechanism, and offer a choice between fixed and floating rates to the customers, while informing them of the pros and cons associated with each option. Such initiatives will also help in improving the ethical standards of banks’ dealing with their customers

Financial Position of the Household Sector:

The household sector is the single largest provider of funding (in terms of personal deposits) to the banking system. In aggregate terms, it holds 46.0 percent of banking system deposits, while it borrows only 12.0 percent of the total loan portfolio. National Income Accounts also reinforces this assessment, as the share of personal savings in total national savings is over 80 percent.

While all these figures clearly indicate the household sector’s significant contribution to the financial sector, a detailed analysis in the context of financial stability is heavily constrained by the lack of appropriate data. The net wealth, or financial position, of the household sector is therefore estimated on the basis of selected indicators including trends in personal deposits of the banking system, individual investments in the stock market, and growth in personal investments in National savings Schemes (NSS). Changes in the consumer loan portfolio of the banking sector are used as the only available indicator of outstanding debt.

Personal Deposits

Personal deposits of the banking sector registered a YoY increase of 19.9 percent during CY07, compared to 18.2 percent in CY06, to reach Rs 1.6 trillion. Strong growth in personal deposits in recent years is also visible from its increasing share in the overall deposits of the banking system. Specifically, the share of personal deposits in total deposits increased to 45.0 percent by end June CY08, in comparison with 42.3 percent at end June CY07, and 40.3 percent as of end June CY03 (Figure 1). This is an encouraging development as the overall deposits of the banking system in recent years have also recorded an average growth of over 18.0 percent during CY03-07. The steady growth in personal deposits is largely attributed to:

(i) record inflows of remittances; and (ii) a sharp increase in per capita income in the wake of strong economic growth in recent years.

1066800147955

Investments in Equity Market

Another indicator of financial health of the household sector is the individual customer’s investments in the stock market. According to statistics from the Central Depository Company (CDC), the number of individual account holders investing in the stock market has reached 41,700 accounts by end CY07, compared to 10,000 at end CY03. The total value of these individual accounts has also grown significantly to reach Rs. 331.7 billion inCY07 against Rs 39.9 billion in CY03 (Figure 2). However, the pace of growth in new individual accounts at CDC has slowed down markedly in CY07, at 6.3 percent in comparison with 13.2 percent in CY06, 121.1 percent in CY05 and 57.0 percent during CY04. Interestingly, despite the lower growth in the number of accounts during CY07, the volume of accounts grew by 51.3 percent against 28.6 percent in CY06; showing increased transactional activities in both new and existing accounts, due to both higher stock prices and increased volume of transactions.

749300125095

Investments in NSS

The Central Directorate of National Savings (CDNS) offers various types of saving schemes for individuals and institutional investors. While all the schemes are open to individual investors, statistics on the proportion of individual investments are not available from CDNS. In order to estimate the growth of personal investments in these instruments, investments in those savings schemes which are offered to individuals investors only are taken into account. These schemes are: Bahbood Saving Certificates (BSC), Pensioner's Benefit Account (PBA) and Prize Bonds. The outstanding amount in these schemes reached Rs 498.0 billion by end June 08, which constitutes 45.9 percent of the outstanding amount in all NSS, instruments i.e. Rs 1,084.0 billion. In aggregate, these schemes increased by Rs 64.3 billion during FY08, which was slightly lower than the increase of Rs 67.7 billion in FY07 (Figure 3). In terms of growth rates, the outstanding amount grew by 14.8 percent during FY08, compared to 18.5 percent in FY07. This slight decline during FY08 is primarily attributed to the fact that the substantial growth in these schemes when they were relatively new is now at more sustainable levels. Also, individuals also invest in other schemes, as BSC and PBA are in particular available for senior citizens/widows/pensioners only. Recent upward revisions of the rate of return on these schemes are likely to attract more investments into these instruments.

12020552540

Following to be discussed in detail in the next lessons

Regulatory Framework for Consumer Financing:

1)

Prudential Regulations for Consumer Financing

2)

Guidelines for Standardization of ATM Operations

3)

Guidelines for Dealing with Customer Complaints

4)

Credit Information Bureau

Redress Mechanisms for Consumer Complaints

Internal Complaint Units/Sections of Banks

Banking Ombudsman

Consumer Protection Department

Banking Courts for Recovery of Loans

The Financial Institutions (Recovery of Finances) Ordinance, 2001

The Payment Systems and Electronic Fund Transfers Act, 2007

The Competition Ordinance, 2007

-33477892991

COSTING / PRICING OF CB PRODUCTS (CONTD…)

SBP PRUDENTIAL REGULATIONS FOR CONSUMER FINANCING APPLICABLE TO ALL BANKS/DFI’S

MINIMUM REQUIREMENTS FOR CONSUMER FINANCING:

General requirements laid down here should be followed by while undertaking consumer financing

These minimum requirements should not in any way be construed to restrict the role of the management to further strengthen the risk management processes through establishing comprehensive credit risk management systems appropriate to their type, scope, sophistication and scale of operations

The Boards of Directors are required to establish policies, procedures and practices to define risks, stipulate responsibilities, specify security requirements, design internal controls and then ensure strict compliance with them

Banking Characteristics

Risk Class

Risk Category

Legislative

Environment

Environmental Risks

Economic

Competitive

Regulatory

Defalcation

Human Resource

Management Risks

Organizational

Ability

Compensation

Operational

Financial Services

Delivery Risks

Technological

New Products

Strategic

Credit

Balance Sheet

Financials Risks

Liquidity

Market

Leverage

Risk is defined as the volatility of a corporation’s market value. The definition that has been selected is as broad as possible. What is of interest is all decisions that may impact on a change in market value

This is consistent with the view that risk management is about optimizing the risk-reward tradeoff– not about minimizing the absolute level of risk

SBP guidelines define financial risk in a banking organization as the possibility that the outcome of an action or event could bring up adverse impacts

Such outcomes could either result in a direct loss of earnings / capital or may result in imposition of constraints on bank’s ability to meet its business objectives

Such constraints pose a risk as these could hinder a bank's ability to conduct its ongoing business or to take benefit of opportunities to enhance its business

-44451905

PRE-OPERATIONS:

Before embarking upon or undertaking consumer financing, the banks / DFIs shall implement / follow the guidelines given below:

The banks / DFIs already involved in the consumer financing will ensure compliance with these guidelines within six months of the date of issuance of Prudential Regulations for Consumer Financing

Banks / DFIs shall establish separate Risk Management capacity for the purpose of consumer financing, which will be suitably staffed by personnel having sufficient expertise and experience in the field of consumer finance / business

They shall prepare comprehensive consumer credit policy duly approved by their BOD (in case of foreign banks, by Country Head and Executive / Management Committee), which shall interlay cover loan administration, including documentation, disbursement and appropriate monitoring mechanism. The policy shall explicitly specify the functions, responsibilities and various staff positions’ powers / authority relating to approval / sanction of consumer financing facility

-106108576200

For every type of consumer finance activity, the bank / DFI shall develop a specific program. The program shall include the objective / quantitative parameters for the eligibility of the borrower and determining the maximum permissible limit per borrower

They shall put in place an efficient computer based MIS for the purpose of consumer finance, which should be able to effectively cater to the needs of consumer financing portfolio and should be flexible enough to generate necessary information reports used by the management for effective monitoring of the their exposure in the area. The MIS is expected to generate the following periodical reports:

Delinquency reports (for 30, 60, and 90, 180 & 360 days and above) on monthly basis

Reports interrelating delinquencies with various types of customers or various attributes of the customers to enable the management to take important policy decisions and make appropriate modifications in the lending program

Quarterly product wise P/L account duly adjusted with the provisions on account of classified accounts. These P/L statements should be placed before the BOD in the immediate next Board Meeting. The branches of foreign banks in order to comply with this condition shall place the reports before a committee comprising of CEO / Country Manager, CFO and Head of Consumer Business

The banks / DFIs shall develop comprehensive recovery procedures for the delinquent consumer loans. The recovery procedures may vary from product to product. However, distinct and objective triggers should be prescribed for taking pre-planned enforcement / recovery measures

The banks / DFIs desirous of undertaking consumer finance will become a member of at least one Consumer Credit Information Bureau. Moreover, the banks / DFIs may share information / data among themselves or subscribe to other databases as they deem fit and appropriate

The financial institutions starting consumer financing are encouraged to impart sufficient training on an ongoing basis to their staff to raise their capability regarding various aspects of consumer finance

The banks / DFIs shall prepare standardized set of borrowing and recourse documents (duly cleared by their legal counsels) for each type of consumer financing

OPERATIONS:

1 .Consumer financing, like other credit facilities, must be subject to the Bank’s / DFI’s risk management process setup for this particular business. The process may include, identifying source of repayment and assessing customers’ ability to repay, his / her past dealings with the bank / DFI, the net worth and information obtained from a Consumer Credit Information Bureau

2 .At the time of granting facility under various modes of consumer financing, banks / DFIs shall obtain a written declaration from the borrower deluging details of various facilities already obtained from other financial institutions. They should allow fresh finance / limit only after ensuring that the total exposure in relation to the repayment capacity of the customer does not exceed the reasonable limits as laid down in their approved policies. The declaration will also help them to avoid exposure against a person having multiple facilities from different financial institutions on the strength of an individual source of repayment

3 .Before allowing any facility, the banks / DFIs shall preferably obtain credit report from the Consumer Credit Information Bureau of which they are a member. The report will be given due weightage while making credit decision

4 .Internal audit and control function of the bank / DFI, apart from other things, should be designed and strengthened so that it can efficiently undertake an objective review of the consumer finance portfolio from time to time to assess various risks and possible weaknesses. The internal audit should also assess the adequacy of the internal controls and ensure that the required policies and standards are developed and practiced. Internal audit should also comment on the steps taken by the management to rectify the weaknesses pointed out by them in their previous reports for reducing the level of risk

5 .The banks / DFIs shall ensure that their accounting and computer systems are well equipped to avoid charging of mark-up on mark-up. For this purpose, it should be ensured that the mark-up charged on the outstanding amount is kept separate from the principal

6 .The banks / DFIs shall ensure that any repayment made by the borrower is accounted for before applying mark-up on the outstanding amount

DISCLOSURE / ETHICS:

The banks / DFIs must clearly disclose, all the important terms, conditions, fees, charges and penalties, which interalia include Annualized Percentage Rate, pre-payment penalties and the conditions under which they apply. For ease of reference and guidance of their customers, banks / DFIs are encouraged to publish brochures regarding frequently asked questions.

For the purposes of this regulation, Annualized Percentage Rate means as follows:

Mark-up paid for the period

360

100

Outstanding Principal Amount

No. of Days

2673985-2774953893185-277495

REGULATION R-1

FACILITIES TO RELATED PERSONS:

The consumer finance facilities extended by banks / DFIs to their directors, major shareholders, employees and family members of these persons shall be at arms length basis and on normal terms and conditions applicable for other customers of the banks / DFIs

The banks / DFIs shall ensure that the appraisal standards are not compromised in such cases and market rates are used for these persons

The facilities extended to their employees as a part of their compensation package under Employees Service Rules shall not fall in this category

Utilization of Clean Loans for Initial Public Offerings IPOs:

While the State Bank’s intent is not to create any undue hindrance in the smooth flow of consumer financing to the borrowers, the banks /DFIs are, however, advised to institute necessary checks, so that clean loans are not used for subscription in Initial Public Offerings (IPOs). In this connection, SBP suggests the following two minimum requirements:

At the time of sanction of a clean consumer loan / credit line, they should obtain an undertaking from the client, that the drawings from the loan account will not be used for subscription in an IPO

They should introduce an internal system, whereby, no cheques, drafts and / or payment instructions will be made for an IPO subscription account from a clean personal loan / credit line account

REGULATION R-2

LIMIT ON EXPOSURE AGAINST TOTAL CONSUMER FINANCING:

Banks / DFIs shall ensure that the aggregate exposure under all consumer financing facilities at the end of first year and second year of the start of their consumer financing does not exceed 2 times and 4 times of their equity respectively. For subsequent years, following limits are placed on the total consumer financing facilities:

788035152400

REGULATION R-3

TOTAL FINANCING FACILITIES TO BE COMMENSURATE WITH THE INCOME:

While extending financing facilities to their customers, the banks / DFIs should ensure that the total installment of the loans extended by them is commensurate with monthly income and repayment capacity of the borrower. This measure would be in addition to their usual evaluations of each proposal concerning credit worthiness of the borrowers, to ensure that their portfolio under consumer finance fulfills the prudential norms and instructions issued by the SBP and does not impair the soundness and safety of the bank / DFI itself.

REGULATION R- 4

GENERAL RESERVE AGAINST CONSUMER FINANCE:

The banks / DFIs shall maintain a general reserve at least equivalent to 1.5% of the consumer portfolio which is fully secured and 5% of the consumer portfolio which is unsecured, to protect them from the risks associated with the economic cyclical nature of this business.

The above reserve requirement will, however, be maintained for the performing portion only of consumer portfolio.

REGULATION R-5

BAR ON TRANSFER OF FACILITIES FROM ONE CATEGORY TO ANOTHER TO AVOID CLASSIFICATION:

The banks / DFIs shall not transfer any loan or facility to be classified, from one category of consumer finance to another, to avoid classification.

REGULATION R-6 MARGIN REQUIREMENTS:

Banks / DFIs are free to determine the margin requirements on consumer facilities provided by them to their clients taking into account the risk profile of the borrower(s) in order to secure their interests. However, this relaxation shall not apply in case of items, import of which is banned by the Government.

Banks / DFIs will continue to observe margin restrictions on shares / TFCs as per existing instructions under Prudential Regulations for Corporate / Commercial Banking (R-6). Further, the restrictions prescribed under paragraph 1.A of Regulation R-6 of the Prudential Regulations for Corporate / Commercial Banking will also be applicable in case of Consumer Financing

State Bank of Pakistan shall continue to exercise its powers for fixation / reinstatement of margin requirements on consumer facilities being provided by banks/DFIs for various purposes, as and when required