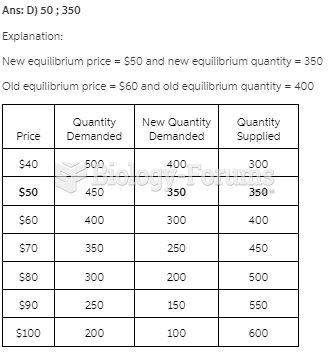

The table above gives information about the labor market in Lantis, a community in which the labor market is perfectly competitive.

If the demand for labor decreases by 200 hours per day, the equilibrium wage rate falls to ________ an hour and the quantity of labor employed ________ hours per day. A) 10; remains at 400

B) 10; decreases to 300

C) 20; increases to 400

D) 5; remains at 200

Ques. 2A market in which the Herfindahl-Hirschman Index is 1,000 is regarded by the Federal Trade Commission as

A) moderately concentrated.

B) concentrated.

C) competitive.

D) monopolistic.

Ques. 3Consider the monopolist depicted in the figure above. The profit maximizing level of output for a single-price monopolist is

A) 7.

B) 11.

C) 13.

D) 22.

Ques. 4In the above figure, the total cost curve is curve

A) A.

B) B.

C) C.

D) none of the curves in the figure.

Ques. 5What is the marginal cost of a good?

What will be an ideal response?

Ques. 6The tables above show the marginal costs and benefits from production of paper. If the market is perfectly competitive and unregulated, the efficient amount of paper will be produced by setting a Pigovian tax of

A) 5 per ton.

B) 10 per ton.

C) 20 per ton.

D) 40 per ton.

Ques. 7Firms are often more efficient than markets as coordinators of economic activity because

A) firms can achieve lower transaction costs.

B) markets cannot coordinate production.

C) firms don't rely on economies of scale while markets do.

D) firm coordination is always more economically efficient than market coordination.

Ques. 8The vertical axis of a graph shows only positive values.

Indicate whether the statement is true or false

Quick Reply

Quick Reply